Fast Cloud-Based Software For Tax Pros

Prepare tax returns faster, easier, and more accurately than ever before with BzPro Tax Software's custom cloud-based software and mobile app. Our user-friendly interface simplifies the tax preparation process, reducing the likelihood of errors and saving you time

Maximize Your Efficiency with

BZPRO TAX SOFTWARE

E-Filing Made Easy

Submit tax returns electronically to the IRS and state agencies, with a fast and secure e-filing process.

Advanced reporting

Generate in-depth reports for clients with just a few clicks, providing detailed insights into their tax returns.

Multi Office Management

Control and manage the most important aspects to run your locations smoothly with the click of a button.

Streamline Your Workflow With BZPRO TAX SOFTWARE's

User-Friendly Interface & Advanced Functionality

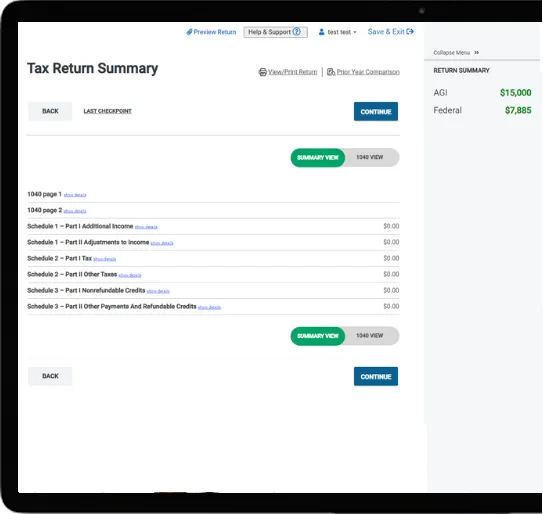

Error Checking

Automatically preform error checks and calculations in real-time, ensuring accurate and error-free tax returns every time.

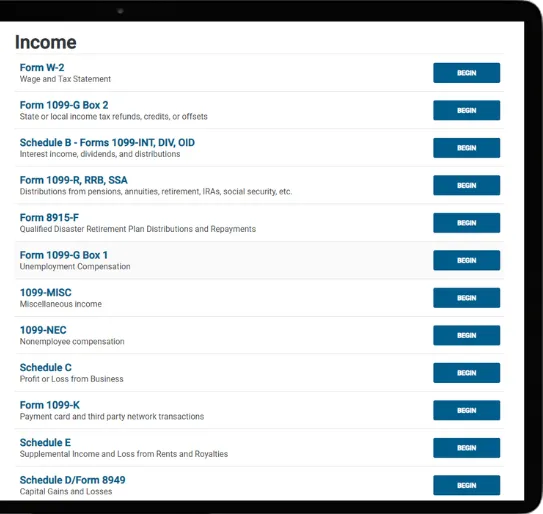

Forms & Schedules

Access over 2,000 federal and state tax forms, schedules, worksheets, and more, all in one place in our form library.

Audit Assistance

Comprehensive audit support & access to audit representation to help you and your clients navigate any potential audit issues.

Cloud Reporting

Automatically preform error checks and calculations in real-time, ensuring accurate and error-free tax returns every time.

Customizable Reports

Our built-in reporting tools allow you to generate custom reports for your clients, providing detailed insights into their tax returns.

Technical Support

We're here to assist you with any questions or issues you may have, ensuring that you always have the support you need.

Streamline Your Workflow With BzPro Tax Software's

User-Friendly Interface & Advanced Functionality

Error Checking

Automatically preform error checks and calculations in real-time, ensuring accurate and error-free tax returns every time.

Forms & Schedules

Access over 2,000 federal and state tax forms, schedules, worksheets, and more, all in one place in our form library.

Audit Assistance

Comprehensive audit support & access to audit representation to help you and your clients navigate any potential audit issues.

Cloud Reporting

Automatically preform error checks and calculations in real-time, ensuring accurate and error-free tax returns every time.

Customizable Reports

Our built-in reporting tools allow you to generate custom reports for your clients, providing detailed insights into their tax returns.

Technical Support

We're here to assist you with any questions or issues you may have, ensuring that you always have the support you need.

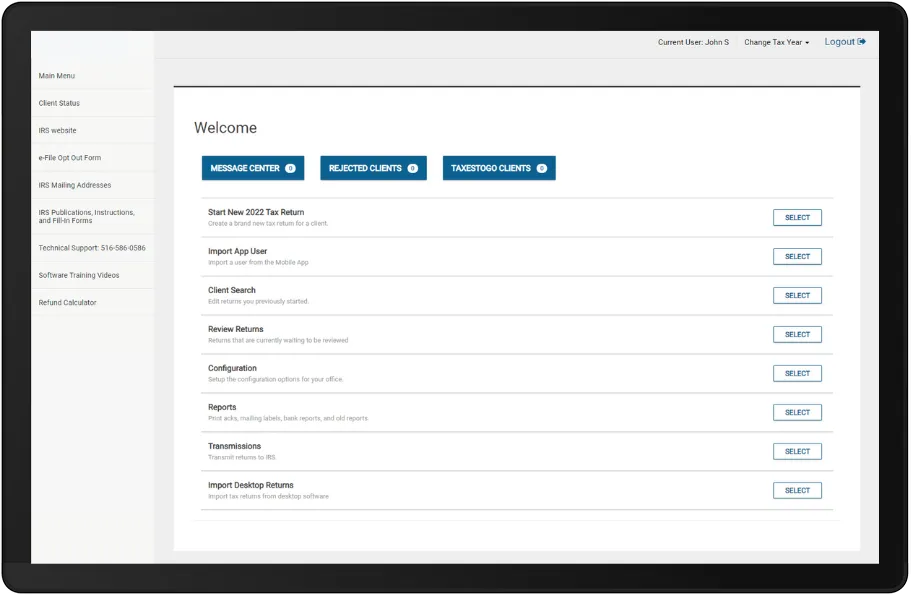

Prepare And File Anywhere, Anytime

Cloud-Based Tax Preparation Software

Our cloud-based software allows you to prepare and file tax returns from any device, providing flexibility and convenience to both you and your customer.

Easy Form Access

Extensive Tax Form Database

Access over 2,000 federal and state tax forms, schedules, worksheets, and more, all in one place within our form library.

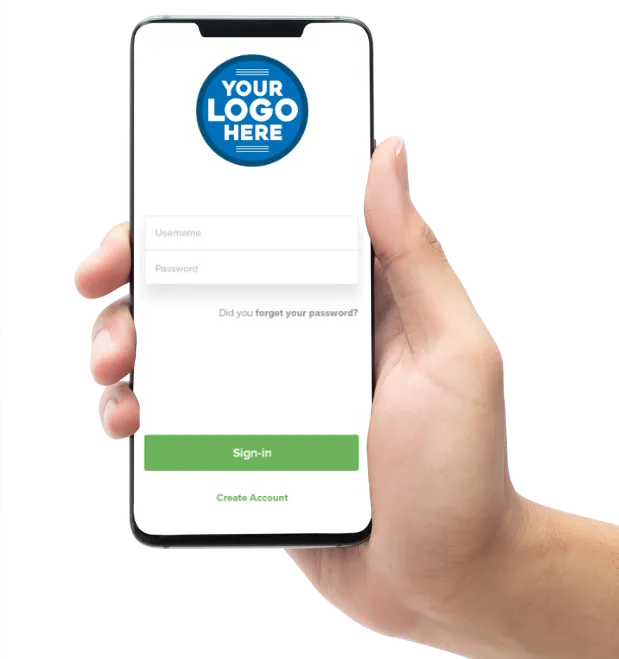

Get Your Own Custom Branded Mobile App

We're Your Mobile Tax Office Solution

Make it as easy as possible for your customers to submit their paperwork with a custom branded mobile app your customers can download. They’ll be able to snap a picture of their paperwork, sign and upload it directly from their mobile device saving both you and your customer valuable time.

Prepare And File Anywhere, Anytime

Cloud-Based Tax Preparation Software

Our cloud-based software allows you to prepare and file tax returns from any device, providing flexibility and convenience to both you and your customer.

Easy Form Access

Extensive Tax Form Database

Access over 2,000 federal and state tax forms, schedules, worksheets, and more, all in one place within our form library.

Get Your Own Custom Branded Mobile App

We're Your Mobile Tax Office Solution

Make it as easy as possible for your customers to submit their paperwork with a custom branded mobile app your customers can download. They’ll be able to snap a picture of their paperwork, sign and upload it directly from their mobile device saving both you and your customer valuable time.

Copyright BzPro Tax Software 2026